As 2019 ended, the backdrop for the energy sector looked relatively solid. Oil prices were up more than 30% in 2019, and future demand appeared firm, as cooling trade tensions between the U.S. and China led many to believe the economy would improve.

It would have been hard for nearly any expert to predict what would happen next. The coronavirus has severely affected the global economy and, in turn, sapped energy demand. At the same time, a price war between Russia and Saudi Arabia has also driven oil prices lower. As a result, the S&P 500 energy sector is down nearly 52% this year, trailing well behind the next biggest sector laggard – financials – which is down 31%.

On the other hand, heading into 2020 few would have predicted utilities would be the best performing sector, down 13% so far this year, but outperforming others due to its defensive nature.

A review of outlooks heading into the year shows how difficult these sector calls are to make. For example, a Barron’s 2020 outlook published in December included sector calls from 10 of Wall Street’s most famous investment strategists. All 10 recommended an overweight to either financials, energy, or both. Our point isn’t to criticize someone else’s recommendations – we know it’s a tough call to make – but to highlight that even the best experts struggle with sector bets.

We believe the outlooks highlight the difficulty of making sector calls and underscore why we avoid sector bets in our portfolios.

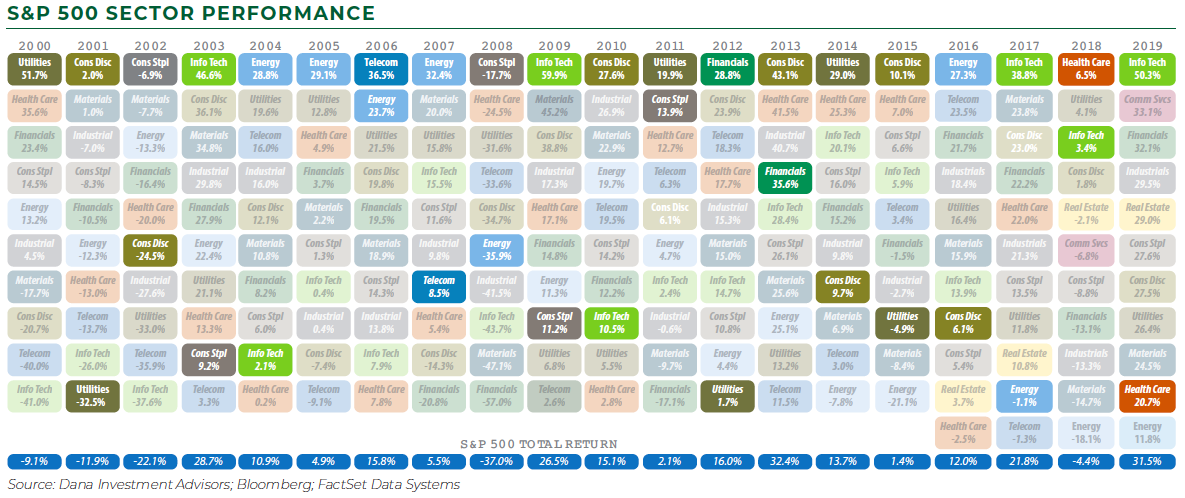

Sector Performance Always Varies Widely

While 2020 highlights how widely sector performance can vary – and how unpredictable sectors can perform – this has always been the case. As the chart below shows, the only consistent element to sector performance is inconsistency.

Dating back to 2000, eight different sectors have been a top-performing S&P 500 sector at least once and six different sectors have been the worst-performing sector during that time frame. Perhaps more important, no sector has consistently been near the top or bottom. The variance in performance between sectors has also been wide, particularly in 2000.

At Dana funds, we try to eliminate sector positioning as a source of risk. Our sector weights match the portfolio’s respective benchmark. This unique risk control helps isolate our active risk to stock selection. Given the variability of sector performance each year, we believe it is easier to make predictions about individual stocks.