Lower quality stocks have outperformed higher quality companies for much of the past year, helped by access to cheap debt and anticipation of an economic rebound. But that may be changing.

Since markets peaked, stocks of higher quality companies – those with low leverage and favorable financial metrics such as high levels of ROIC* and ROE** – have outperformed. We believe there are a few reasons that trend could continue.

First, relative valuations of higher quality names look more attractive. This is particularly true for small caps, where a risk-on environment fueled a rally by lower quality names in 2020 and early this year. As of April 30th, small cap companies with the lowest levels of ROE traded at 9.8 times revenue and almost 5 times book value, according to data from Jefferies1.

Conversely, companies in the top quintile when ranked by ROE trade at only 2 times revenue and 3 times book value.

Beyond valuations, a couple of other factors could favor higher quality companies in the coming quarters. One of those is that the cost of debt is likely to increase. Access to cheap credit has likely been one of the reasons lower quality companies outperformed in 2020 and early 2021. Intuitively, this makes sense. A company with a weaker or more leveraged balance sheet is more dependent on debt, so they benefit when that debt is cheaper. From this perspective, it wasn’t surprising to see lower quality companies outperform as credit spreads tightened to their narrowest level since 2007.

But when the cost of servicing debt goes up stocks of higher-quality companies tend to outperform those of lower quality companies, because rising debt costs are less of a burden to high-quality businesses. Given where credit spreads and interest rates are today, we would expect those debt costs to tick up, which could favor higher quality stocks.

A third factor that augurs well for higher quality companies is the threat of higher inflation. This is partially because rising inflation can lead to rising interest rates, and in turn, rising debt costs. But there’s more: In an environment where costs are rising, a company with a stronger balance sheet is more equipped to absorb them.

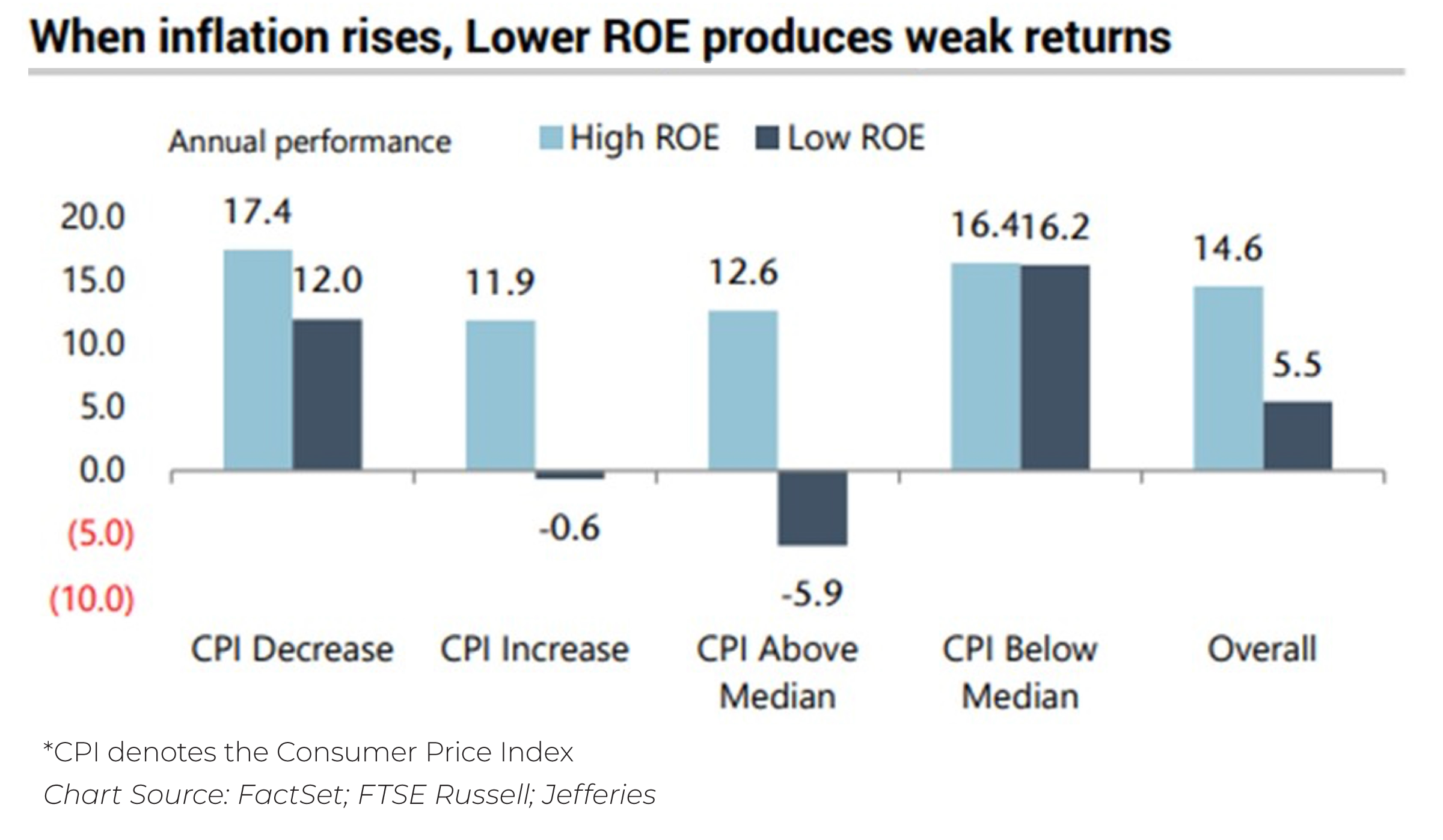

The chart below shows how this trend has played out in previous periods, with stocks of companies in the top quintile of ROE outperforming those in the lowest quintile substantially when the consumer price index, a gauge of inflation, is above median. (These higher quality companies also outperformed in periods of relatively small price increases and overall.)

We Believe Quality Always Counts

At Dana, high levels of ROIC or ROE and lower leverage aren’t just something our portfolio managers prefer; they are table stakes for making it into our portfolios. We take a high-quality approach, which means we favor companies with strong balance sheets, low levels of debt and high levels of free cash flow generation. We take this approach because a company with a stronger balance sheet is better positioned to weather an economic downturn. Companies with stronger balance sheets and greater free cash flow*** generation are also better positioned to execute on strategic growth initiatives, because they are not reliant on cheap credit to fund them.

Over full market cycles, higher quality stocks have outperformed lower quality ones, largely because of their ability to hold up when markets are volatile or the business and economic environment is challenging. If we are entering another environment where the strength of these companies is in favor, we would welcome the change.

* Return on Invested Capital (ROIC) is the amount of money a company makes that is above the average cost it pays for its debt and equity capital.

** Return on Equity (ROE) is a measure of financial performance. It is calculated by dividing net income by shareholders' equity.

*** Free cash flow assesses how efficiently a company generates cash. It is found by subtracting a company’s capital expenditures from its cashflow from operations.

1Source: Jefferies. JEF SMid Cap Themes - Can Valuations Momentum Coexist We Think So (May 19, 2021). P8 DeSanctis, S., Lockenvitz, E.