One of the most-common questions we receive is: why do we manage our portfolio’s in a sector-neutral fashion (sector-neutral meaning the process of rebalancing our sector weightings to match those of the benchmark)? After all, why would an active manager want to look like the index? Why not overweight certain indices where we are finding the most-attractive opportunities?

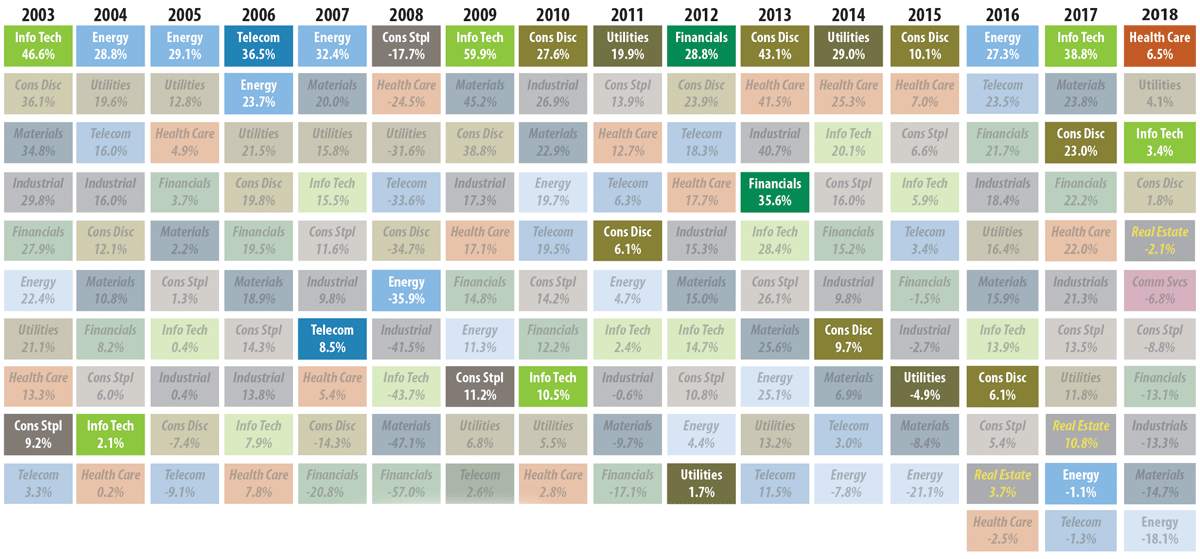

The short answer is that we prefer to focus our time and effort on picking what we believe are the very best stocks within each sector and industry. There is a considerable amount of randomness and cyclicality that goes into relative sector performance; thus, we believe it makes more sense to focus on bottom-up stock selection instead. Observe the following matrix which displays the S&P 500’s top-performing sector in each calendar year, and where that sector ranked the following year:

In 10 of the 16 calendar years, the top-performing sector went on to rank in the bottom 50% of sectors the following year. This illustrates the extreme difficulty of predicting sector performance, and begs the question: why would any manager believe they have an edge in making sector bets?

Consider this example. Coming out of the bursting of the dot-com bubble, from 2004 to 2007, oil prices rose from mid-$30s per barrel to over $100. As a result, energy was either the first- or second-best-performing sector each year during this time frame. Portfolio managers who had overweighed the sector were reassured of their seemingly-above-average intelligence! Over the following years, these money management teams likely owned companies in the exploration and production (E&P) space which were developing state-of-the-art horizontal drilling and hydraulic fracturing techniques which revolutionized the American energy landscape. Unfortunately, this “energy renaissance” ultimately contributed to a global surplus of oil. Prices fell materially over the following years, and still have not recovered to levels seen in 2007-2008. Since 2012, within the S&P 500 Index, the energy sector has ranked in the bottom three sectors in six of the past seven years.

A sector-neutral approach helps prevent us from falling into the psychological biases of trend-chasing and overconfidence which are very common, and often hard to avoid, in the investment industry. Furthermore, it immunizes our clients from the additional volatility that can result from dramatic sector rotations and shifts in investor sentiment.

To learn more about this aspect of our process, as well as our other unique approaches such as equal-weighted position sizes, we encourage you to explore our process overview, available for download here.