Asset managers are all sunshine and roses when the market is riding high, but in a bear market you need to understand how your manager is working for you. We want to share details about our disciplined investment process, because the market is experiencing high volatility and sudden downturns.

Our “superprocess” consists of quantitative modeling to rank potential investments and qualitative research into business models and management, while also integrating ESG factors. We add to this a disciplined adherence to sector and industry weightings so that we’re not unintentionally allowing human bias to affect your investments.

In this post, we’ll offer an overview of each of these steps, and in future posts we’ll dive deep on each one. With each case study or one-on-one explanation from our portfolio managers, you’ll better understand why we call our process a superpower.

Step 1: Idea Generation Via Quantitative Rankings

Our portfolio managers have varied backgrounds, but they are all data people. Our quantitative model isn’t a black box it is an efficiency tool for our team.

We gather financially material information from public filings, of course. But we add to that layers of data that can also be material, from sources like Glassdoor and Spring Pond, to help us understand how firms value their talent and culture. We look at artificial intelligence to determine what ESG issues come up in press releases and in internal documents. We’ve built a system that (importantly) does not eliminate companies. It ranks them along various metrics, and sometimes those metrics don’t all point in the same direction.

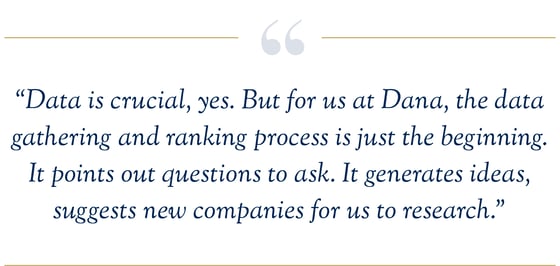

Data is crucial, yes. But for us at Dana, the data gathering and ranking process is just the beginning. It points out questions to ask. It generates ideas, suggests new companies for us to research.

Step 2: Fundamentals Drive Investment Decisions

OK. Ideas and questions have arisen from our broad-based number crunching. Where do we go from there? How do we go from, “this software company looks promising,” to, “the potential returns for this software company are not fully reflected in its stock price”? Enter, fundamental research.

We dig into companies and ask questions about everything from the business model and how it’s differentiated in its industry, to the approach to sustainability and the clean energy transition. We dig in deeply to understand their earnings projections and the assumptions underlying them. If one of our data sources reports that a company has a toxic work environment, and the other that it’s heaven on earth, we ask tough questions to get to the bottom of the discrepancy, and that goes for any risk factor that might overshadow otherwise sunny management guidance.

Step 3. Discipline Drives Choice to Sell

The questions begin with our fundamental research, but they don’t end there. We continually review our investments to determine whether they still meet our standards. Is management executing on the plans they elucidated for us when we initiated our position? Is the risk/reward opportunity still attractive, given ever-changing industry dynamics?

In keeping with our policy of embracing of data, we utilize several models to evaluate each security we hold. We look at how each elevates issues within a company, and then determine, given its sector and industry, whether it still belongs in our portfolio.

Step 4. Structure Drives Risk Control

The key to our risk controls is the structure we maintain in each portfolio. We remain convinced that there is no consistent way for any investment professional to time the market. So we stay sector neutral, regardless of economic conditions, because timing those conditions is impossible. Each stock holding is equally weighted as well, which means we are more likely to notice poor stock performance within sectors and industries. We don’t “chase winners,” which helps us keep human bias out of your investments.

Finally, we remain fully invested, we don’t hold cash. You hire us to run a strategy, so we use our expertise to choose the best stocks in that strategy. No need to keep any cash that needs to be backed out in order to properly measure performance.

Our sector-neutral approach and equal-weighted position sizes have historically helped us avoid becoming overconfident in any one sector or position. This discipline limits situations where human biases and egos could create unnecessary risks in the portfolio.

We believe Dana’s time-tested investment process focusing on high-quality companies trading at a discount to peers can provide strong relative performance in sustained bear markets.

We view quality in terms of:

- Qualitative: proven management teams, ESG factors and sustainable competitive advantages.

& - Quantitative: Strong cash flows, higher-than-index returns and profitability

Call us to talk over your investment plans and to learn how we can help you build a resilient portfolio.